Navigating the AI frontier in financial reporting

By embracing innovation while managing risk, auditors can shape a future in which technology strengthens trust, transparency and value in financial information, writes Ross Donohoe

The explosion in public awareness of artificial intelligence (AI) since 2022 has been seismic.

As a concept, AI became openly accessible to everyone when OpenAI released ChatGPT in November 2022. OpenAI’s competitors were quick to respond with the release of their own AI models shortly thereafter.

Now, three years on, there is real excitement about what AI could mean for our future.

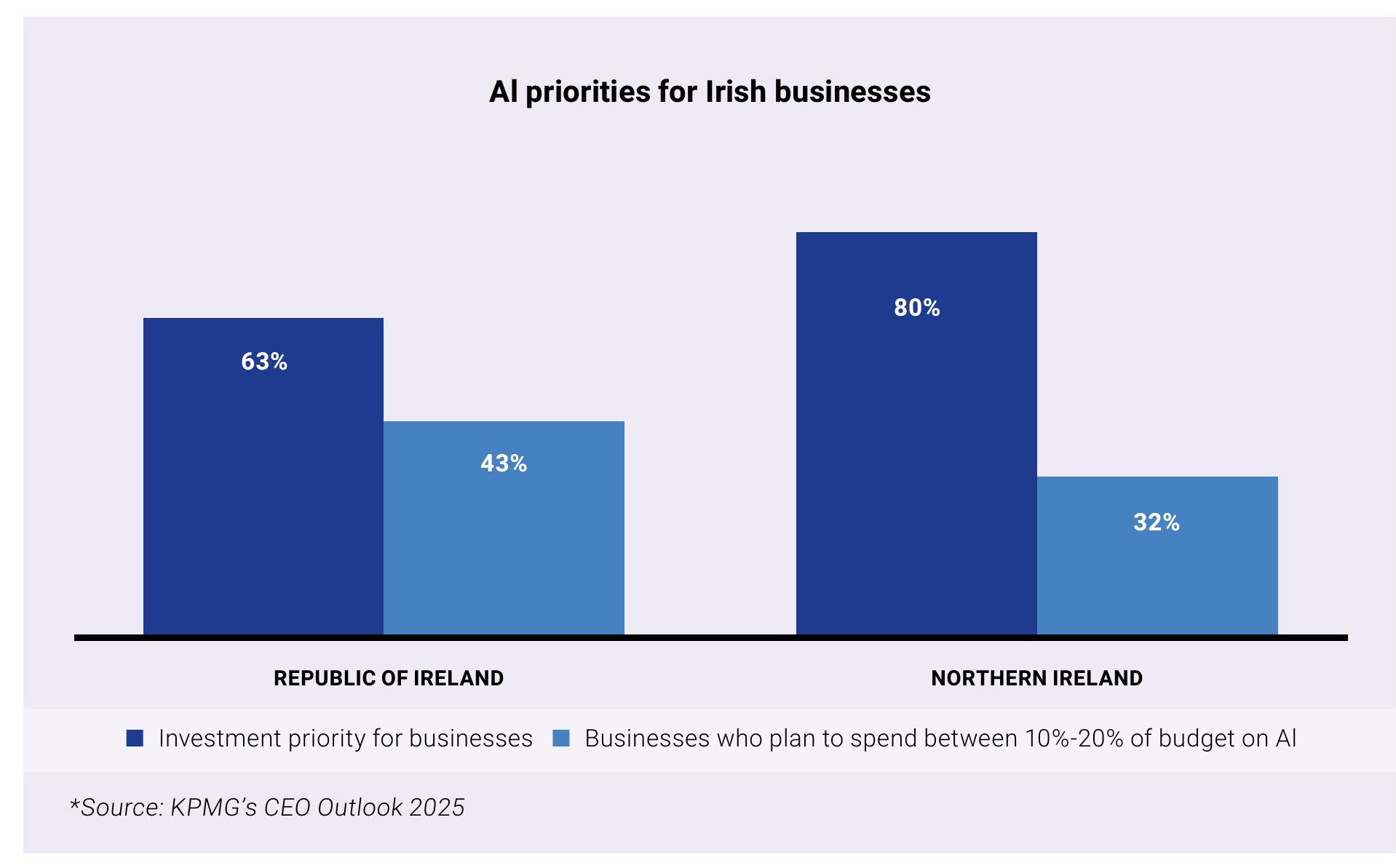

Published in October, KPMG’s CEO Outlook 2025 found that AI is a top investment priority for 63 percent of entities in the Republic of Ireland and 80 percent in Northern Ireland.

Forty-three percent of leaders in the Republic of Ireland and 32 percent in Northern Ireland expect to spend 10-20 percent of their budget on AI in the year ahead.

AI: implications for business

So, what does this mean for businesses, both in Ireland and around the world, when it comes to implementing AI in their financial reporting processes? And how might it impact a company’s statutory audits?

For most businesses, automation and the use of technology within the financial reporting process is not a new concept.

For decades, companies have made use of a multitude of automated programmes to assist in completing repetitive tasks such as, for example, posting automated journal entries.

Until now, these programmes have automated rules-based tasks, requiring little or no judgement on the part of the operating programme.

The coding behind these programmes is transparent and can be audited; the input-output is easily observable.

AI on the other hand, is completely different. It has been described as a “black box” of sorts.

While the input-output is observable, AI’s internal decision-making process is not easily accessible.

A key feature of AI programmes is that they learn from data input patterns and can change the way in which they make decisions based on past experiences.

In short, AI tools are constantly evolving. As a result, one AI tool might give two completely different answers to the exact same question.

This is not the case with traditional machine learning and algorithms. It presents a challenge for businesses in their day-to-day monitoring, and for external auditors tasked with obtaining sufficient appropriate audit evidence in relation to the operability of AI tools.

Overcoming implementation challenges

As is par for the course these days, implementing any new process in a business is far from a plug-and-play solution. This is especially true when it comes to AI tools.

Careful consideration must be given to how AI tools will process data. Data protection laws mandate that the processing of any personal data must be fair and transparent.

Given the black box nature of AI tools, this presents a challenge for businesses required to adhere to local data processing laws.

In 2024 and 2025, the Data Protection Commissioner publicly announced various inquiries into how the likes of Meta, Google and X (formerly Twitter) process personal data with respect to their new AI tools—though no findings have been published to date.

Another challenge in using AI rears its head in the form of “hallucinations”. Hallucinations occur when large language models (LLMs) present incorrect, fabricated or nonsensical information as if it were a statement of fact.

Hallucinations are a known limitation in LLMs such as ChatGPT, M365 CoPilot and Grok, to name a few.

Perhaps one of the more infamous cases of such a hallucination occurred less than a year after the public release of ChatGPT when lawyers in a US law firm submitted citations to a district judge in Manhattan.

The document cited six legal cases invented by the LLM as part of an aviation injury claim. Given the novelty of AI at the time, the case gained notoriety around the world and serves as a reminder that AI is far from infallible.

Consideration must also be given to the need to educate and train employees on the appropriate use of AI tools, and their limitations.

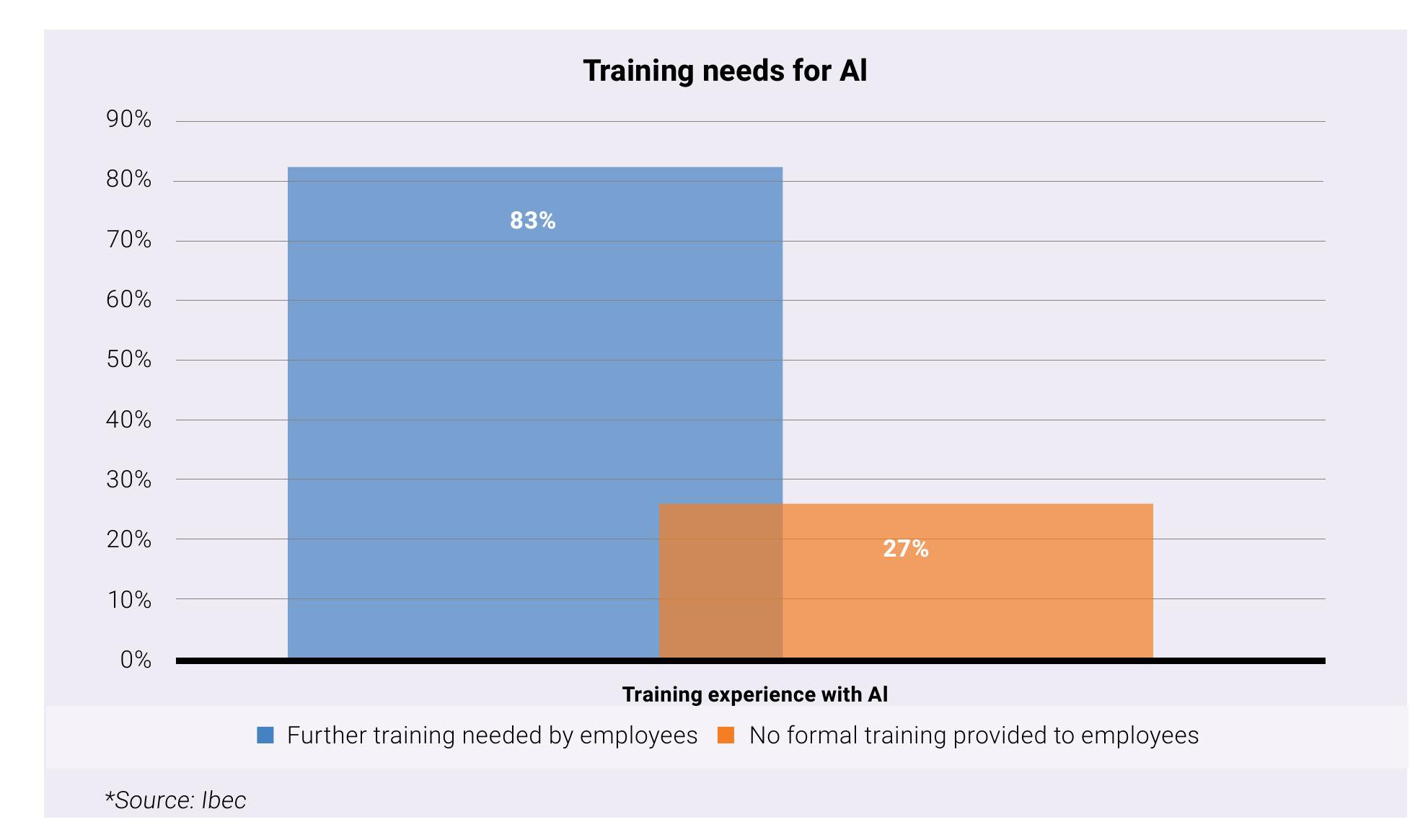

Research conducted by business group Ibec found that, in July 2025, 40 percent of employees used AI in their workplace tasks compared to 19 percent in August 2024.

Strikingly, 83 percent of the employees surveyed by Ibec said they needed more training in AI while 27 percent reported receiving no formal training in the use of AI tools.

The finding that one-in-four employees have received no formal training in AI should be a concern for business leaders as it is crucial that users understand how AI tools work and, more importantly, what their limitations are.

To address these challenges, it is vital that businesses adopt AI tools carefully, rather than diving in without proper consideration. Businesses should liaise with internal and external stakeholders as part of their adoption of AI.

Boards and sub-committees will need to get involved in drafting and approving acceptable usage policies for AI.

Terms and conditions agreed between businesses and their suppliers and customers will likely require amendments to allow for the use of new AI tools— particularly with regard to the processing of personal data.

AI in financial reporting and auditing

Prior to implementing AI tools within the financial reporting process, consideration needs to be given to its impact on the annual statutory audit and other assurance services.

It is important for businesses to discuss the full scope of their planned use of AI tools with their external auditors as this will represent a significant change in the financial reporting process for auditors.

In circumstances where automation is fundamental to an entity’s internal controls over financial reporting, auditors will often complete extensive testing of general IT controls and IT application controls related to the system.

As noted in the introduction to this article, these applications have traditionally been rules-based systems in which the decision-making element is observable.

Auditors will need to consider the impact of AI tools on their ability to obtain audit evidence.

Audit opinions may need to be modified if sufficient appropriate audit evidence cannot be obtained due to the black box nature of AI tools. This is why it is crucial that businesses and their auditors traverse the new technology together.

Financial reporting and auditing: AI use cases

The real benefit of AI models is that they can process vast amounts of data and become experts in the subject matter they are trained on. The potential use cases for AI are vast.

From an operational perspective, AI could assist in pre-screening tasks such as customer credit applications, making an initial decision for human review.

However, as Rumman Chowdhury—Twitter’s former head of machine learning ethics, transparency and accountability—has pointed out, AI tools can develop biases based on the data on which they are trained.

Chowdhury noted the policy of redlining in 1930s Chicago whereby banks would deny lending to minorities. This bias would likely be identified by an AI system as part of its training and could be perpetuated further.

A well-thought-out AI governance model and staff training could potentially overcome this type of hurdle, however.

From a financial reporting perspective, there are many uses for AI. We might see AI conducting regular reviews of companies’ aged debtors to determine if there are signs that the debtor may be credit-impaired, for example, requiring provisioning on the balance sheet.

Perhaps AI may even one day prepare a company’s annual draft financial statements, allowing the business more time to improve the overall quality of the reporting contained within the financial statements.

It is not unreasonable to assume this scenario could become a reality, if AI is fully integrated within the financial reporting process.

From an auditor’s perspective, we are already seeing the benefits of AI tools when carrying out our statutory audits.

KPMG has developed AI transaction scoring (AITS) which analyses up to 100 percent of revenue transactions recorded during the year and identifies their risk of misstatement as low, medium or higher.

This tool significantly improves audit quality as it analyses the population and directs auditors to test revenue transactions with a higher risk of misstatement rather than the traditional statistical sampling approach which could see hundreds of revenue transactions tested.

We have also seen the development of financial statement analyser tools which review draft financial statements, identifying potential inaccuracies such as totting errors and internal inconsistencies.

These tools are just the start of what might be to come. Looking ahead, with the integration of client-side AI tools, we could see the advent of AI-assisted narrative drafting, variance commentary and financial statement note disclosure assembly.

On the audit side—as systems and controls mature, allowing businesses to generate quantitative and qualitative data—we could see the advent of a continuous, real-time audit process, whereby audit procedures take place throughout the year, not just at year-end.

Particularly for listed entities, the possibility of a continuous audit has tangible benefits—in particular, the potential to eliminate the crunch period known as the “busy season” when businesses and auditors race to issue financial statements and audit reports thereon to the capital markets.

None of this will happen without significant investments, however.

AI tools: the road ahead

Ultimately, the successful adoption of AI in financial reporting hinges on collaboration between businesses, auditors, regulators and technology providers.

By embracing innovation while remaining mindful of all associated risks, businesses and auditors can shape a future in which technology strengthens trust, transparency and value in financial information.

The next chapter for AI in audit is just beginning and those who prepare thoughtfully will be best positioned to lead.

Ross Donohoe is an Associate Director in Financial Services Audit at KPMG Ireland